The global urea market plays a pivotal role in ensuring food security, as urea remains the most widely used nitrogen fertilizer worldwide. With agriculture driving demand and industrial applications expanding, leading urea producers are at the forefront of innovation, sustainability, and large-scale production. Below, we provide an in-depth analysis of the top urea companies in 2025, highlighting their production capacity, market strategies, and contribution to global supply.

Global Urea Market Overview

Urea is an essential component in global agriculture, accounting for over 50% of nitrogenous fertilizer use. The market has seen steady growth due to:

- Rising population and food demand

- Expansion of agricultural land

- Growing adoption of high-efficiency fertilizers

- Increased industrial applications in plastics, adhesives, and resins

In 2025, the market size is expected to exceed USD 65 billion, with leading producers in the Middle East, Asia-Pacific, and Europe dominating exports.

Leading Urea Producers in 2025

1. Qatar Fertiliser Company (QAFCO) – Qatar

- Capacity: Over 5.6 million metric tons annually

- Strengths: World’s largest single-site producer of urea

- Highlights: Operates advanced ammonia and urea plants; strong focus on clean energy integration

2. Saudi Basic Industries Corporation (SABIC) – Saudi Arabia

- Capacity: More than 4.5 million tons per year

- Highlights: Diversified chemical giant with strong export network

- Sustainability: Investing in carbon capture and green hydrogen to reduce emissions

3. CF Industries – United States

- Capacity: Over 9 million tons of nitrogen products (urea and ammonia)

- Strengths: Major supplier in North America with global exports

- Innovation: Leading research in low-carbon urea production

4. National Fertilizers Limited (NFL) – India

- Capacity: Approx. 3.6 million tons annually

- Highlights: Key government-owned fertilizer producer in India

- Market Role: Ensures food security for India’s vast agricultural base

5. Indian Farmers Fertiliser Cooperative (IFFCO) – India

- Capacity: Over 4 million tons annually

- Strengths: One of the world’s largest cooperatives

- Contribution: Supplies affordable fertilizers to millions of Indian farmers

6. Yara International – Norway

- Capacity: Around 3.5 million tons of urea

- Strengths: Global footprint across Europe, South America, and Africa

- Focus: Sustainable farming and climate-smart agriculture solutions

7. China National Petroleum Corporation (CNPC) – China

- Capacity: Over 10 million tons of nitrogen fertilizers (urea included)

- Highlights: One of the largest state-owned enterprises in China

- Strengths: Vertical integration with oil and gas operations

8. Koch Fertilizer – United States

- Capacity: Approx. 3.5 million tons of urea

- Highlights: Global distribution network with plants across North America

- Focus: Efficiency in logistics and long-term partnerships with distributors

9. Fauji Fertilizer Company (FFC) – Pakistan

- Capacity: Over 2.5 million tons annually

- Highlights: Pakistan’s largest urea producer

- Contribution: Ensures agricultural productivity and food security in South Asia

10. Aljabal Holding – UAE

- Highlights: A rapidly growing supplier of urea and other petrochemicals

- Strengths: Strong global distribution in Asia, Africa, and the Middle East

- Expansion: Investing in logistics hubs to streamline fertilizer exports

Regional Market Leaders

- Middle East: Qatar, Saudi Arabia, and the UAE dominate exports due to natural gas availability.

- Asia-Pacific: China and India lead consumption and production.

- North America: U.S. producers benefit from shale gas resources.

- Europe: Yara International focuses on sustainable fertilizers for advanced agricultural systems.

Sustainability in Urea Production

Environmental regulations and climate change concerns are pushing companies to adopt green ammonia and carbon-neutral urea technologies. Leaders like SABIC, Yara, and CF Industries are investing in:

- Carbon capture and storage (CCS)

- Hydrogen-based urea production

- Energy-efficient ammonia synthesis

Supply Chain & Export Trends

- Major Exporters: Qatar, Saudi Arabia, China, and the UAE

- Key Importers: India, Brazil, and African nations

- Trends:

- Increased adoption of digital trading platforms

- Greater investment in port and storage infrastructure

- Strategic partnerships for global fertilizer distribution

Challenges Facing Urea Companies

- Price Volatility – Linked to natural gas feedstock

- Environmental Concerns – Nitrogen runoff and greenhouse gas emissions

- Geopolitical Tensions – Supply chain disruptions in fertilizer trade

- Sustainability Pressure – Demand for eco-friendly fertilizers

Future Outlook 2025–2030

- Rising global demand will sustain high production capacity.

- More investment in green urea projects across Europe and the Middle East.

- Expansion of digital agriculture platforms integrated with fertilizer companies.

- Greater regional cooperation to stabilize global fertilizer supply chains.

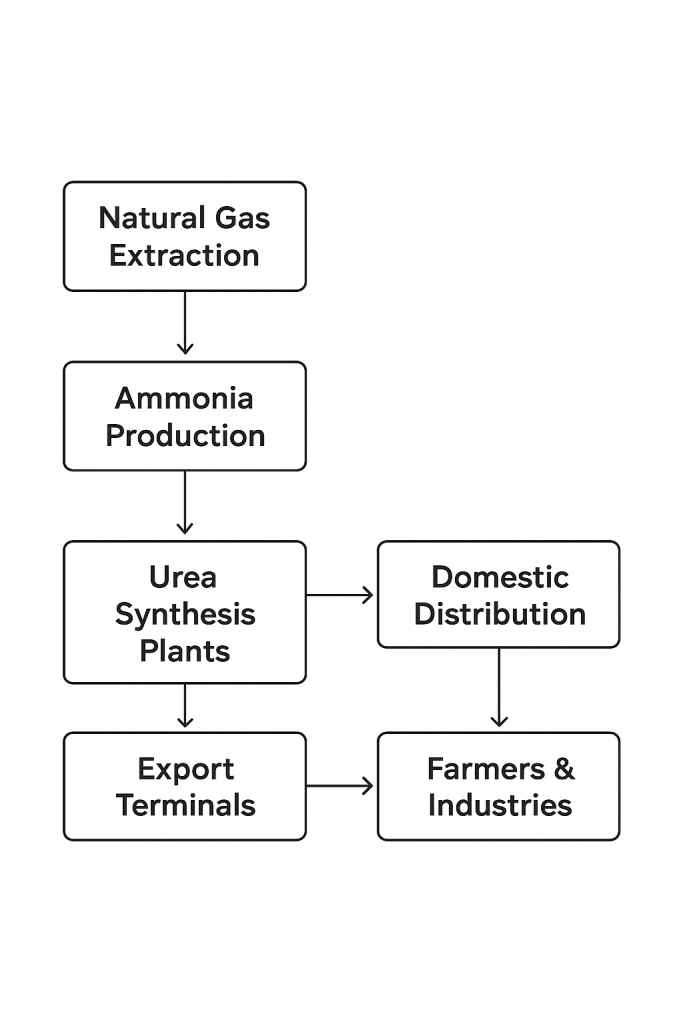

Suggested Diagram – Global Urea Supply Chain

Conclusion

The top urea companies in 2025 are not only expanding production but also reshaping the future of agriculture with sustainable practices and global distribution networks. From industry giants like QAFCO and SABIC to emerging players like Aljabal Holding, these companies ensure the world’s farmers have access to the most critical input for food production, while aligning with sustainability goals.